8 months Ago

8 months Ago

That is the case, for example, of the Netherlands, where Dutch mortgage lending has outpaced growth in mortgage loans on average in the entire euro area since the fourth quarter of 2023. Meanwhile, lending volumes fell, but the rate of decline was slower than in other European areas.

Demand driven by house prices, earnings and interest rates

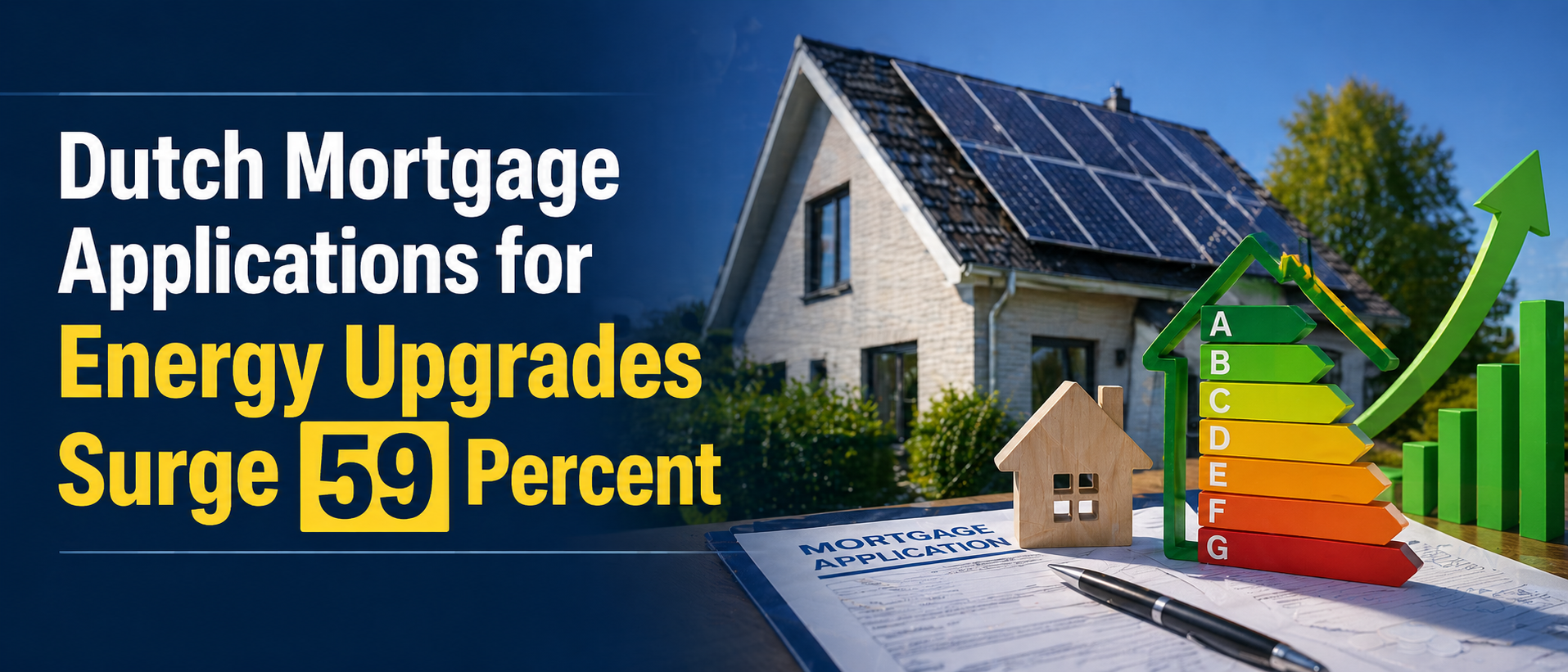

A number of different elements have contributed to the elevated demand for mortgage applications. There was faster house price growth as well as better wage growth, lower interest rates and stronger population growth. Dutch house prices rose by 9.3 percent on average in June, national data out this week showed.

One other trend that stands out is an increasing appetite on the part of borrowers for fixed-interest terms of shorter durations. Of all new residential mortgages, 5- to 10-year fixed-rate deals now account for more than half. That is a shift from prior years, say before 2023, when interest rates on the long-term fixed rates were lower.

Higher Saving Mingling With Lower Payment Account Balances

A year earlier, in June, savings for Dutch households were €429 billion or 10 percent higher. The fall in sign and pay accounts was offset by a €6 billion to €110 billion drop in regular payment balances, but they are still almost much lower than the €133bn figure recorded three years ago.

The move indicates that consumers are now savvy about rising interest rates. As the interest rate in current accounts is zero, many people transfer their money into savings accounts and earn returns. In the face of wage growth, overall bank balances haven't actually risen as hoped, with these shifting saving habits accounting for a lot of it.